The Carbon Majors Report published in 2017 showed that 100 active fossil fuel producers including ExxonMobil, Shell, BHP Billiton and Gazprom were linked to 71% of industrial greenhouse gas emissions since 1988. This shocked the world, and was a strong catalyst in the growing consciousness of organisations’ contribution to global warming and their lack of corporate responsibility.

Reporting on their environmental and social impacts through Environmental, Social and Governance (ESG) reporting was seen as an important step in understanding an organisation’s impacts and fostering a culture of operational transparency and change. As part of the Environmental category, carbon reporting allows companies to measure and understand their carbon impact, which is crucial in developing effective strategies to reduce emissions and reach ever-expanding Net Zero targets. The transparency of carbon impact disclosure helps build trust with stakeholders, including customers, investors, and regulators who are demanding more accountability and action on environmental issues. In addition to just ‘good practice’, many jurisdictions now require carbon reporting as part of their regulatory framework, and it is anticipated that more will follow suit. It is also being increasingly understood that this unchartered territory of publicising organisational affairs, whilst daunting to many, can actually lead to cost savings, innovation, and competitive advantage in the market - which further drives the prevalence of carbon reporting and cements the practice of corporate responsibility and transparency.

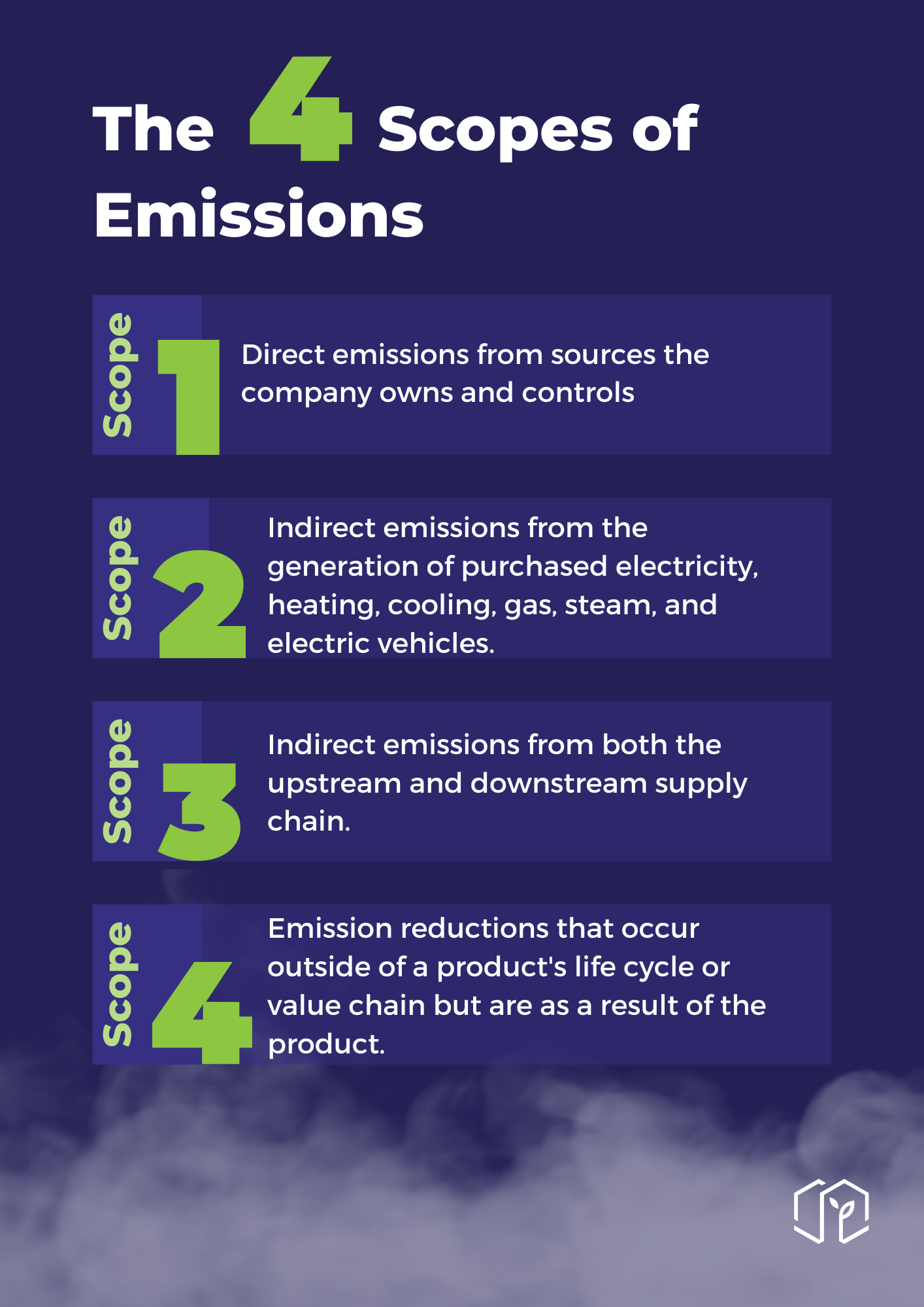

Despite having been introduced in 2001, many professionals have only recently become acquainted with the leading international carbon accounting standard, the Greenhouse Gas (GHG) Protocol. The GHG protocol categorises an organisations direct and indirect emissions into three broad scopes, Scope 1, 2, and 3, as follows:

-

Scope 1 Emissions: Direct emissions from sources the company owns and controls (e.g. company-owned facilities or vehicles)

-

Scope 2 Emissions: Indirect emissions that come from the generation of purchased electricity, heating, cooling, gas, steam, and electric vehicles.

-

Scope 3 Emissions: Indirect emissions from both the upstream and downstream supply chain.

Scope 1 and 2 emissions reporting now forms the backbone of most corporate sustainability strategies, with Scope 3 emissions being increasingly understood and measured. Yet, whilst organisations are just getting to grips with these three scopes, a broader perspective is increasingly being recognised as necessary to capture the full environmental impact of a company.

Scope 4 emissions

Conversations are ramping up about a fourth class of emissions - Scope 4 emissions, or most commonly described as ‘avoided emissions’. These emissions signify the emission reductions that occur outside of a product's life cycle or value chain but as a result of the product. This could involve products or services that actively reduce emissions, like low-temperature detergents, fuel-saving tires, energy-efficient ball bearings, or teleconferencing services. But why do Scope 4 Emissions Matter? The integration of Scope 4 emissions into carbon accounting is important to provide companies with a more holistic view of a company's short- and long-term impacts. It provides a forward-thinking and proactive approach to carbon management, unlike the 'reactive' approach of Scopes 1 to 3 (where the aim is to reduce existing emissions), Scope 4 encourages 'proactive' steps to help prevent emissions from occurring in the first place. This is positive as it will help organisations understand the potential savings from investing in sustainable projects, products, services or methodologies and how best to reduce their environmental footprint.

Why ‘avoid’ over ‘reduce’?

A grim reality that we are increasingly having to face is that even with our our current optimistic Net Zero targets in place at both organisational and national levels, the rate at which we are burning through our carbon budget means that we are still on a trajectory above the 2 degrees celsius warming scenario and have little chance of staying below 1.5 degrees.

We have lost the luxury of time and unfortunately cannot continue with our current ‘reduction’ mindset, from the ubiquitous “plant a tree” initiatives to the race to produce complicated carbon capture technologies. We now have to prioritise ‘avoidance’ over 'reduction' and ensure that we prevent emissions from being released from the outset. This additional layer of carbon reporting will encourage organisations to both use carbon-saving products and methodologies, as well innovate them. When used in conjunction to the reduction of direct and indirect emissions, organisations can truly understand their impacts, undergo thorough scenario analysis and effectively strategise their sustainable growth.

As a home-grown example, Preoptima’s software focusses on “emissions avoidance using Carbon Twins”. We use Carbon Twins and whole life carbon analysis in building design and construction to mirror the impacts of design choices from the earliest concept stages, thus ensuring that every building project starts from an optimised, low carbon foundational design and stays on that trajectory throughout the technical design and construction phases. Our focus on embodied carbon in particular ensures that we prevent emissions from being released from the outset instead of focussing on operational savings down the line, as is commonly done in the industry.

The risks of Scope 4 emissions

Whilst the recognition of Scope 4 emissions is positive, it has potential to act as a double-edged sword. Firstly, avoided emissions should not be seen as an ‘easy out’ for Scope 1, 2 and 3 emissions (or as a means to ’offset’ these emissions), as they are completely unrelated to the GHG Protocol and avoided emissions are not captured within these scopes. In addition, there is no generally accepted methodology for calculating and reporting on Scope 4 emissions, presenting risks of significant variation in the calculation and communication of Scope 4 emissions and the potential of greenwashing.

Overall, there is no need to panic and start reporting on Scope 4 emissions tomorrow, but given the fast pace of industry standards and best practice, it is definitely important to start thinking about how and when you would integrate Scope 4 emissions into your reporting structure. The business landscape is continuously evolving according to our global pressures - and we have to adapt with it!